Our Best Intel: Consumer AI

|

|

|

Morning Consult captures the leading indicators of consumer intent every day, across global markets, and delivers them through always-on intelligence and custom research built for speed, confidence, and growth. Leaders from the world's largest companies, equity research firms, hedge funds, and the Federal Reserve rely on our 30,000 daily survey interviews in 100+ countries covering more than 5,000 brands, economic indicators, and risk metrics. See the research in action. We last looked at consumer AI back in January. This week's briefings track how the category has shifted since then. |

|

|

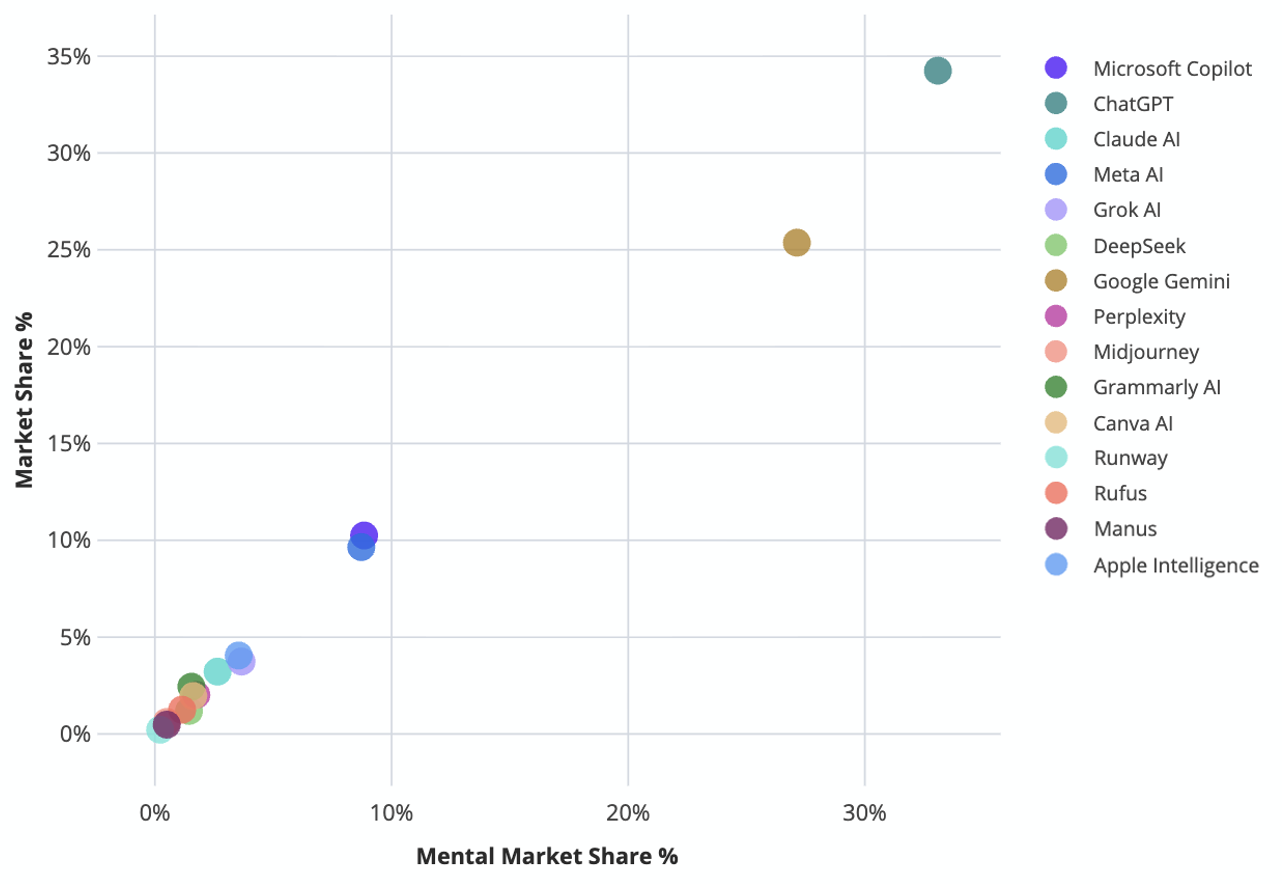

BOTTOM LINE UP FRONT: Consumer AI has matured into a category with two dominant brands and one breakout challenger. Gemini and ChatGPT continue to bracket the category — Gemini consolidating its hold on search-replacement and information utility, ChatGPT defending the conversational and creative lane. Their leadership is now structural rather than competitive: neither gained ground on the other this wave. The breakout story is Claude — +13pp awareness, +5pp mental penetration, +4pp active use over four months, with gains concentrated almost exclusively in the $100K+ and post-graduate segments where premium-tier conversion happens. Distribution-led brands (Apple Intelligence, Meta AI) continue to lose AI mind-share. Switching inertia is hardening — “happy with current AI” rose to ~29%, the only barrier moving meaningfully upward. The category is settling into a more mature shape. In this briefing, we use the Category Advantage research framework to measure how consumers consider different types. A few terms you should know: |

- Mental Market Share (MMS) measures a brand’s "mental availability"—how often it comes to mind, compared to competitors, when consumers think of buying in a category

- Category Entry Points (CEPs) are the specific needs, motivations, situations, or feelings that trigger a consumer to consider a product category and the brands within it

- Network Size refers to the average number of distinct usage occasions or buying situations that consumers mentally associate with a brand

|

|

|

How The Category is Developing |

Two leaders, two lanes, structural stability. ChatGPT and Gemini hold ~85% and ~75% awareness respectively, with ~67% and ~61% Mental Penetration — both in the territory where consumers reliably encounter the brand when an AI moment arises. Their CEP-association profiles are now distinct rather than overlapping. Gemini leads on Quick Answers (~53%), Health Info (~51%), Translation (~49%), and Researching topics (~53%) — the search-replacement and utility lane. ChatGPT leads on Rewriting (~51%), Learning new skills (~49%), Creating content (~41%), Boredom/chat (~40%), and Kids’ Homework (~38%) — the conversational, creative, and personal-life lane. Neither leader gained share against the other this wave; both consolidated their respective lanes. Claude is the breakout story. Awareness rose from ~27% to ~39% (+13pp), Mental Penetration from ~10% to ~15% (+5pp), active use from ~5% to ~9% (+4pp) — the only major brand growing on every conversion measure. The gains concentrate where Claude’s strategic positioning would predict: $100K+ earners (active use 8.5% → 17.1%, +9pp), post-graduates (7.3% → 15.0%, +8pp), and Bachelor’s-degree holders (5.2% → 10.3%, +5pp). Awareness rose +22pp among 65+ adults — the steepest demographic gain in the dataset — though active use among that segment remains modest (~3%). Distribution-led brands continue to lose AI mind-share. Apple Intelligence awareness fell from ~39% to ~35% (-4pp), Mental Penetration -3.5pp, active use -1.1pp. Meta AI active use dropped from ~26% to ~22% (-4pp). Microsoft Copilot held flat (-0.3pp on active use), but its conversion of awareness into past-month use remains the lowest among the major brands at ~36%. The thesis that preinstallation alone would build durable AI brand preference is not playing out — these brands have ecosystem reach but are not capturing AI moments at the rate their footprint would suggest. Task specialists are losing ground in “AI tool” mind-share. Grammarly awareness -2.9pp, Canva AI -2.1pp. Both remain leaders on their specific occasions (Grammarly with ChatGPT on Rewriting; Canva on Creating content), but they are losing footprint as AI tools in consumer minds even where they retain their original task-brand recall. The bundling of “AI” with general-purpose chatbots is hardening into a default association that pulls awareness away from category-specific players. Grok and DeepSeek have gained awareness without conversion. Grok awareness +7.5pp to ~38%, but active use only +1.5pp; DeepSeek awareness +5.0pp to ~30%, active use +0.9pp. Both brands are entering more consumers’ mental maps but have not yet earned a place in their behavioral stack — the inverse pattern from Claude, where awareness gains are translating into use. |

|

|

Featured Report: America 250 Corporate Sponsorship Report |

Do consumers support corporate sponsorship of America 250? Is backlash a possibility? Which audiences are most likely to engage? This report provides clear takeaways on those questions, and also features a related analysis of how corporate sponsorship of President Trump’s second inauguration impacted brand perceptions. |

|

|

Economic sentiment: AI users remain meaningfully more optimistic than the U.S. adult average — 49% expect to be better off financially in 12 months vs 36% gen pop. Twelve-month and five-year business-condition expectations have softened across the past year. The audience is still optimistic, but less unambiguously so than at the start of the year. Psychographics: This remains the most concentrated early-adopter audience in any consumer category MC measures. 66% identify as “first to try new technology” (+35pp vs gen pop), 53% strive for high social status (+26pp), 73% pay premium for ease (+23pp). The “too much technology = bad” sentiment that rose through late 2025 has reversed in early 2026 — AI users are reconciling with technology as it embeds rather than recoiling from it. Status, novelty, and ease remain the three activation currencies. Media footprint: AI users over-index on use of Reddit (+31pp), X (+30pp), Spotify (+27pp), WhatsApp (+27pp), and Snapchat (+27pp). Sports media over-indexes 20–28pp on nearly every league. Podcasts are oversaturated (86% of AI users vs 49% gen pop). |

|

|

The category structure is constant; segment weighting shifts within it. 18–34: ChatGPT remains dominant for the cohort that adopted it first. Claude awareness rose +8pp here but active use remains in single digits. Gemini gained mental penetration with this group (+6pp) — the age divide that defined the first wave is starting to soften. 45–64: The most actively reshuffling segment. ChatGPT held active use but lost ~3pp Mental Penetration. Claude awareness rose +15pp, active use +5pp. The work-utility spine cohort is opening up to non-leader options. $100K+: The most strategically meaningful segment movement. ChatGPT active use fell from ~68% to ~63% (-6pp); Grok fell from ~17% to ~11% (-7pp); Copilot fell ~4pp. Gemini rose +4pp; Claude rose +9pp to 17%. The premium audience is consolidating around Gemini and Claude. Parents: Most stable segment for ChatGPT (active use ~58%, essentially flat). Family-life CEPs — kids’ homework, meal planning — anchor parental loyalty more than any other use case. |

|

|

More Accurate Than Wall Street |

Over the past 60 days, Morning Consult data outperformed the Wall Street consensus on 44 confirmed earnings calls— predicting the correct direction of the earnings surprise and the stock moved to confirm it. These results come from our ongoing partnership with Maiden Century, a leading alternative data platform. Maiden Century applies Morning Consult Intelligence data — which tracks daily consumer sentiment for thousands of brands across 40+ countries — to build quarterly earnings models and rank their accuracy against dozens of competing data sources. |

|

|

Claude has earned its third lane in the segments that matter. The premium audience — $100K+, post-grad, Bachelor’s — is where subscription conversion happens, and Claude’s gains in this audience are the most strategically meaningful signal in the dataset. Strategic conversations about challenger AI brands should now treat Claude differently from Grok, Perplexity, and DeepSeek. Claude has crossed into the consideration set of the audience that pays. Distribution alone does not build AI brand preference. Apple Intelligence and Meta AI continue to lose AI mind-share despite preinstallation across hundreds of millions of devices. Microsoft Copilot’s awareness-to-active-use conversion is the lowest among major brands. The data is consistent: ecosystem reach generates trial, but does not generate the brand association that drives sustained use. Investment in occasion-specific positioning will outperform additional distribution muscle. Switching inertia is hardening — the window is closing. “Happy with the AI I currently use” rose +4.3pp to ~29%, the only barrier moving meaningfully upward this wave. Combined with structurally stable trust barriers (privacy ~29%, AI distrust ~26%) and Mental Penetration consolidation among the leaders, the category is approaching the maturation threshold where new entrants face exponentially harder displacement work. Brands that have not yet claimed a CEP territory will find the market less responsive each quarter. Emotional connection is softening across the leaders. ChatGPT emotional connection declined from 4.06 to 3.65 (1–7 scale), Gemini from 3.80 to 3.35, Microsoft Copilot from 3.19 to 2.71. Mental Penetration held; active use held; what changed is how warmly users feel about the tool. AI is becoming utilitarian rather than affectionate. This raises the bar for differentiation: capability is table stakes, but feature parity does not generate emotional reattachment. Brand-experience signals — voice, personality, trust frames, identity — are now where differentiation lives. Trust friction is structural, not transient. Privacy concerns and AI distrust held flat at ~29% and ~26%. The barrier is foundational and concentrated in 65+, $100K+, and Northeast segments. Trust messaging — privacy proof points, transparent data practices, visible safety frames — remains a high-leverage investment in the segments where premium revenue concentrates. |

|

|

Most research tells you what already happened. Morning Consult tells you what's coming. |

Most organizations are making decisions on research that wasn't built for the speed at which consumers and markets change today. Data is slow. Insights are fragmented. By the time analysis reaches leadership, the moment has already passed. Morning Consult changes that. From brand health and spending behavior to economic sentiment and political trends, we track the signals that move markets every day, so your team sees shifts coming before they show up in your numbers. |

|

|

One Always-On Consumer Signal. Two Complementary Solutions:

1. Intel Platform: AI-driven consumer and market research platform that transforms daily consumer surveys into clear, stakeholder-ready insight - helping leaders continuously monitor change and move from data to decision, faster.

2. Custom Research: On-demand market research built on the most advanced survey research technology to deliver solutions that are fast, scalable, cost-efficient, and built for action. |

|

|

|