Leaders from the world’s largest companies, equity research firms, hedge funds, and the Federal Reserve rely on Morning Consult’s 30,000 daily survey interviews in 45 countries covering more than 5,000 brands, economic indicators, and risk metrics. Category Advantage measures the drivers of brand strength by capturing mental availability and emotional closeness among competitors.

This week's briefings will cover the U.S. automobile category. Read our research on this category here. |

|

|

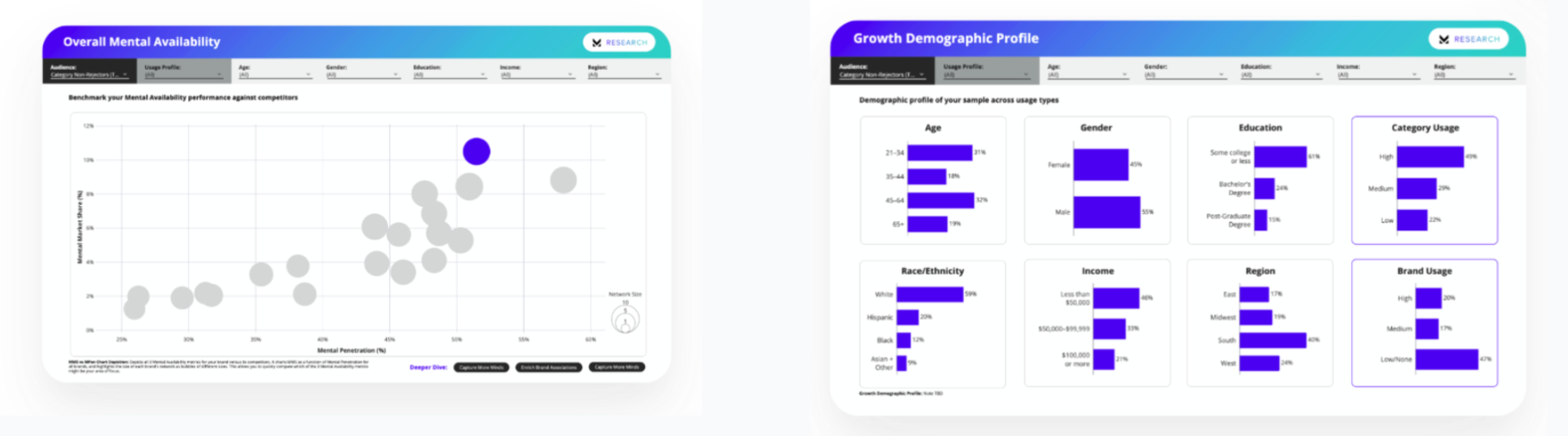

BOTTOM LINE UP FRONT: Toyota is the mental availability leader in the U.S. auto category -- recalled by more buyers, across more purchase triggers, than any other brand. With an 8.1% Mental Market Share and 67% mental penetration, it outpaces Ford (5.7%, 55%) and Honda (5.9%, 64%) at the total level, and leads all brands in purchase intent at 35%. But Toyota's strength is structurally concentrated in functional and financial triggers -- reliability, maintenance cost, and first-time ownership. It under-indexes on status, reward, and the thrill of driving. That is not an immediate threat, but it limits Toyota's ability to expand into more premium territory in the category. The next phase of Toyota's growth requires defending the reliability fortress while building an emotional layer that earns the right to charge more and mean more. |

|

|

Toyota leads the category on every core mental availability metric. Its Mental Market Share of 8.1% is the highest of any brand -- ahead of Honda (5.9%), Ford (5.7%), and Chevrolet (5.6%). Its mental penetration of 67% means two-thirds of all auto buyers link Toyota to at least one purchase trigger, versus 55% for Ford and 45% for Tesla. Its network size of 708 -- the average number of purchase triggers linked to Toyota per person who recalls it -- is the broadest in the category, 100 points ahead of Honda (608) and 265 points ahead of Tesla (443). Purchase intent confirms the lead. 35% of auto buyers say they would definitely or probably purchase a Toyota -- the highest of any brand and well ahead of Honda (29%), Ford (26%), and Chevrolet (24%). Intent is strongest in the West (43%) and among younger buyers aged 18-34 (41%), two segments with above-average category growth potential. The structural advantage is real, but narrowly anchored. Toyota's green cells on the Mental Advantage grid cluster tightly around reliability (+10), low maintenance cost (+8), first-car and teen driver moments, and cost reduction triggers. Its red cells -- under-indexing brands by more than five points -- cluster around status (+/- -19), thrill of driving (-10), and reward (-11). Toyota dominates rational entry. It underperforms in aspirational entry. |

|

|

Reliability and cost control are Toyota's mental fortress. The top CEPs where Toyota leads are: low maintenance cost (30% salience), safety ratings (26%), circumstantial need for commute or job (26%), second car as responsibilities expand (24%), first car purchase (22%), and breakdown-driven upgrades (23%). These are high-frequency, emotionally grounded triggers that together represent the majority of category volume. Toyota's ownership of this cluster is its single greatest competitive asset. The West is Toyota's strongest regional market. Mental Market Share reaches 9.3% in the West -- the brand's highest regional score -- driven by strong hybrid and EV adjacency, cultural alignment with reliability and environmental progress, and high mental penetration (69%). The Midwest (7.2%) and South are competitive but show lower network size (645), suggesting shallower associative depth in durability-heavy markets where Ford and Chevrolet hold structural advantages. Younger buyers and lower-income segments are Toyota's volume base. Mental penetration holds above 67% among under-34 buyers and lower-income segments -- both groups where first-car ownership, maintenance cost sensitivity, and financial pragmatism drive entry. Purchase intent among 18-34 buyers is 41%, the highest of any segment, making this cohort critical to long-term loyalty compounding. |

|

|

Toyota's biggest structural vulnerability is not competitive -- it is positional. No rival currently threatens its reliability leadership. The gap is emotional: Toyota is not the brand buyers turn to when they want to reward themselves, signal status, or feel the thrill of driving. The status and reward deficit is measurable. On 'wanting to reward myself,' Toyota scores -11 on the Mental Advantage grid -- one of the deepest negative scores in the category. On 'wanting a car that elevates my status,' it scores -13. On 'wanting to feel a sense of thrill,' it scores -10. BMW (+11 on status), Mercedes-Benz (+14 on status), and Porsche dominate these associations. Among high-income buyers ($100K+), where these triggers carry more weight, Toyota's Mental Market Share of 7.2% is its weakest income segment -- and mental penetration drops to 63%. This limits Toyota's ability to play in more premium spaces. Buyers who associate a brand with status, reward, and aspiration are less price-sensitive and more likely to trade up within a brand family. Toyota's under-indexing on these triggers means it leaves premium pricing power on the table -- particularly in Lexus-adjacent segments where the brand could credibly reach if the emotional narrative were stronger. |

|

|

What's Blocking Conversion |

Toyota's recall is not its constraint. Where market share under-indexes relative to mental share, the gap is friction -- not memory. Three barrier clusters are most relevant: Purchase experience friction in high-density markets. The East is Toyota's weakest conversion region. Despite strong brand recall, dealer experience distrust, negotiation anxiety, and competitive clutter suppress conversion. A digital-first buying journey, transparent pricing, and financing pre-approval integration are the levers here -- not more advertising. Perceived 'not premium enough' among high-income buyers. In the $100K+ segment, Toyota's reliability is assumed rather than valued. The emotional gap -- weak status and reward associations -- becomes the conversion barrier. Competitive premium alternatives (BMW, Mercedes-Benz, Lexus) capture the aspirational share that Toyota's functional positioning does not reach. EV credibility vs Tesla in innovation-forward segments. Among younger buyers and in the West, Tesla's Mental Market Share of 5.0% and purchase intent of 21% represent meaningful competitive pressure in the technology and innovation space. Toyota leads on hybrid dependability but does not yet dominate the autonomous or full-EV narrative. The risk is being seen as reliable but not leading. |

|

|

Measure the true drivers of brand strength |

Built on validated principles of brand-driven growth and powered by Morning Consult’s industry-leading sampling technology, Category Advantage allows you to: |

- Uncover Category Entry Points directly tied to mental availability. See the specific needs, occasions, and triggers that drive purchase decisions in your category, and how strongly your brand is linked to them.

- Pinpoint Growth Opportunities to direct investment toward the moments and consumer segments with the greatest potential to grow your brand.

|

|

|

The reliability fortress must be defended first. Toyota's core advantage -- deep associations with long-term reliability, low maintenance cost, and first-time ownership -- is its largest mental moat. Any strategy that dilutes these associations in pursuit of aspiration will weaken the foundation. Reinforcement of warranty visibility, ownership economics, and durability proof-points is non-negotiable, particularly in the Midwest and South. Emotional modernity is the growth unlock. Toyota cannot credibly pivot to pure performance or luxury positioning -- nor should it. The opportunity is a narrower repositioning: 'smart success,' 'progress without compromise,' or 'confidence feels good.' This builds emotional lift without abandoning the rational base, and creates a bridge to premium segments where Lexus can carry the heavier aspirational load. Own practical innovation -- not just reliable engineering. Category consumers are more comfortable with autonomous technology than the general population. Toyota should lead on hybrid and EV dependability, position driver-assistance features as 'safety you can trust,' and emphasize technology that enhances reliability rather than replacing it. The message is not 'Toyota is innovative' -- it is 'Toyota makes technology you can count on.' Fix conversion where recall is already strong. In the East, where awareness is high but conversion lags, the investment priority is purchase experience -- digital journey simplification, financing transparency, and inventory visibility -- not awareness spending. Every dollar spent on reach in a market where Toyota already has 67% mental penetration is underperforming relative to friction removal. |

|

|

Leaders from the world’s largest companies, equity research firms, hedge funds, and the Federal Reserve rely on Morning Consult’s 30,000 daily survey interviews in 45 countries covering more than 5,000 brands, economic indicators, and risk metrics. One Always-On Consumer Signal. Two Complementary Solutions:

1. Intel Platform: AI-driven consumer and market research platform that transforms daily consumer surveys into clear, stakeholder-ready insight - helping leaders continuously monitor change and move from data to decision, faster.

2. Custom Research: On-demand market research built on the most advanced survey research technology to deliver solutions that are fast, scalable, cost-efficient, and built for action. |

|

|

|